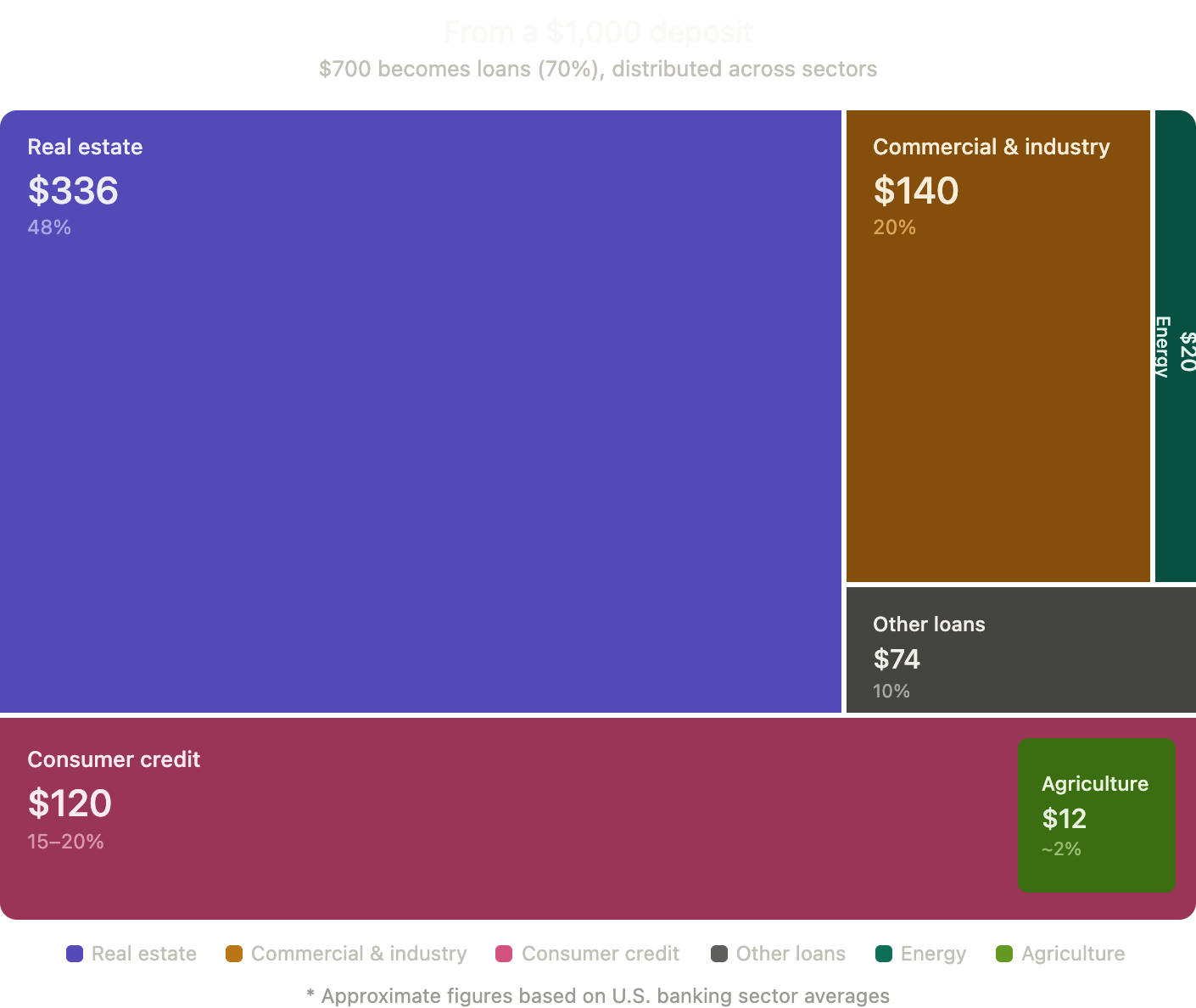

When someone deposits $1,000, nearly 70% of it becomes part of the lending that shapes the real economy:

What your bank does with your money

Most people think a bank account is just storage. But the moment deposits arrive, they become active, flowing into loans that shape neighborhoods, infrastructure, opportunity, and even the environmental conditions people live with.

Banks decide where that money goes next. And those decisions quietly determine:

- who gets to build a home

- which neighborhoods get reliable electricity

- who pays the highest energy bills

- which technologies become affordable

- where small businesses grow

- which communities become resilient to changes

- who gets to build a home